A hardware startup can survive difficult engineering problems, build a working prototype, and even attract investor attention. Yet many products still fail before reaching real commercial scale. The reason is often far less visible than the technology itself. Between prototype completion and production launch, supply chains can in fact shift fast enough to break timelines, destroy cost structures, and delay entire product rollouts.

Hardware Startups Often Collapse During the Production Window, Not the Prototype Stage

Most general assumptions believe that once startups can secure investors and build working products, they are bound to succeed. Unfortunately, that is not always the case.

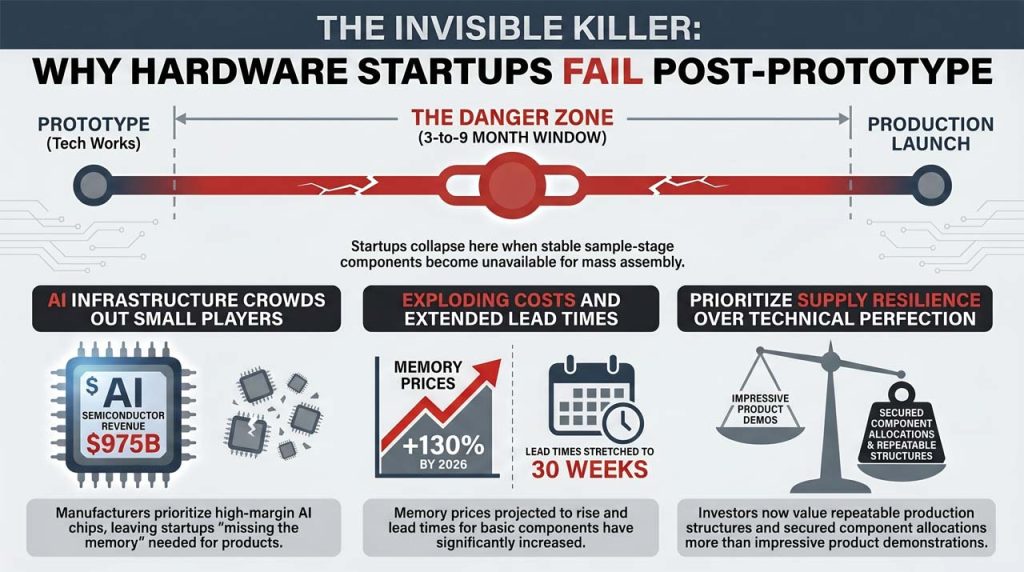

Because for many hardware founders, the most dangerous period begins after the prototype works instead. A product may perform successfully during the testing stage. But they can still fail commercially if critical components become unavailable before production begins.

Sung Bong Kang, CEO of NEWNOP Group, has worked across electronics development, automotive systems, manufacturing operations, and quality engineering before leading the company.

He believes one of the biggest operational risks facing hardware startups today is supply-chain instability during the transition into mass production.

“The most realistic failure factor is supply chain change,”

Kang told KoreaTechDesk as discussions on prototype-to-production challenges continued.

“Especially for key IC components, supply may look stable during the sample stage.

But during the three to nine months needed for mass production, supply interruptions, global issues such as war or logistics problems, and rapid price increases can occur.”

His observation reflects a growing structural challenge across the global electronics industry. In recent months, semiconductor manufacturers have increasingly prioritized AI infrastructure demand, tightening supply availability for many downstream hardware products.

According to Deloitte’s 2026 semiconductor outlook, global semiconductor revenue is projected to approach USD 975 billion in 2026, driven heavily by AI-related demand. Yet, at the same time, Deloitte noted that shortages in consumer memory products have already emerged as suppliers redirect capacity toward higher-margin AI infrastructure markets.

Memory Shortages and Component Delays Are Reshaping Hardware Economics

The pressure is no longer limited to advanced AI chips alone. It is now spreading into broader hardware supply chains involving memory, passive components, analog chips, and power management systems commonly used by startups and smaller device manufacturers.

Research firm Gartner estimated that combined DRAM and SSD pricing could rise by as much as 130% by the end of 2026. Gartner also projected that rising memory costs may reduce global PC shipments by 10.4% and smartphone shipments by 8.4% compared with 2025 levels.

Reuters separately reported that growing AI infrastructure demand has absorbed large portions of global memory supply, pushing semiconductor manufacturers to prioritize higher-margin enterprise markets. Intel CEO Lip-Bu Tan stated in the report that some smaller companies were now “missing the memory” required to complete products.

This creates a serious imbalance for startups.

Large OEMs can often secure allocation agreements earlier through purchasing scale and long-term contracts.

But as smaller hardware startups operate with weaker bargaining power, shorter purchasing visibility, and tighter cash flow, technically functional products may still become commercially impossible to manufacture at the expected cost.

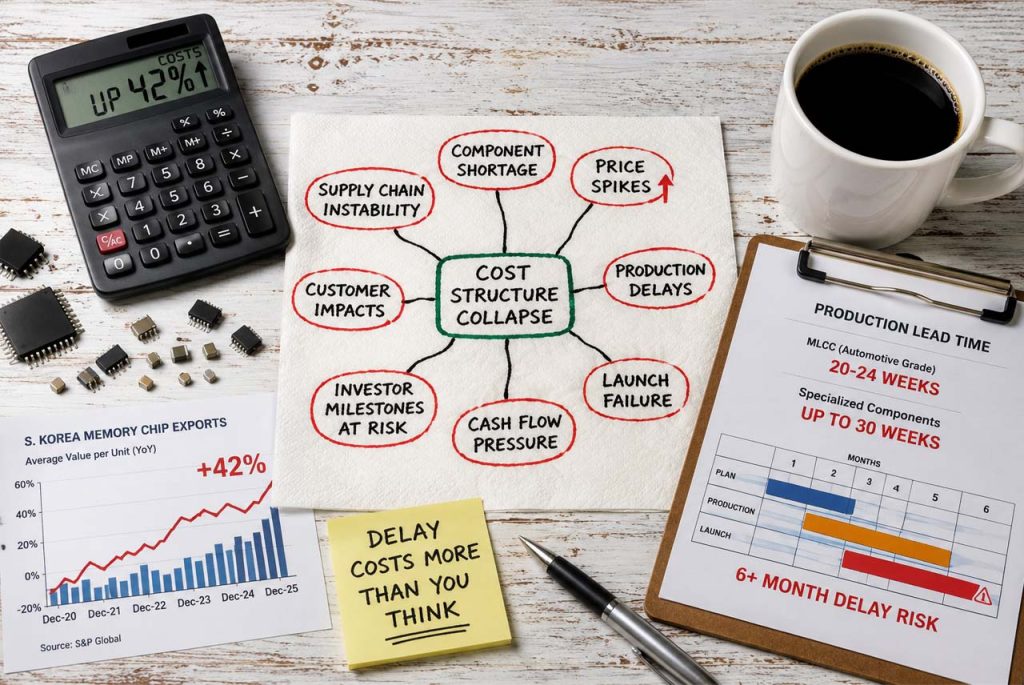

The Hidden Risk Is Not Just Shortage, But Cost Structure Collapse

Moreover, the sudden component shortages create not only a procurement problem for hardware startups. They also trigger broader operational damage across pricing, scheduling, and production planning.

Kang explained that startups frequently underestimate how quickly rising component prices can destabilize the economics of an entire product launch.

“In some situations, cost structures collapse, production is delayed, and product launches fail,”

he said.

This risk has become increasingly visible across Asia’s electronics supply chain. S&P Globalreported that the average value per unit of South Korean memory-chip exports rose 42% year over year in December 2025, reaching the highest level recorded since at least 2016.

At the same time, Korean electronics media outlet ETNews reported that global shortages are now affecting multilayer ceramic capacitors (MLCCs), chip resistors, inductors, motor drivers, and power semiconductors. Some automotive-grade MLCC lead times reportedly reached 20 to 24 weeks, while certain specialized products required up to 30 weeks of waiting time.

Now, for startups operating on limited runway, these delays can become existential.

A six-month production delay may affect investor milestones, customer contracts, distribution agreements, and future fundraising plans simultaneously.

Global Supply Shocks Are Now Affecting Startup Manufacturing Timelines

The supply-chain environment has also become increasingly vulnerable to geopolitical disruption and raw-material instability.

According to Yonhap News Agency, South Korea relies heavily on Qatar for helium imports used in semiconductor and display manufacturing. Korea also depends heavily on Israeli bromine imports used in semiconductor processing materials.

ETNews further reported that prices for petrochemical-based semiconductor process materials rose 20% to 30% during the first quarter of 2026 amid rising Middle East instability and energy-market pressure.

Meanwhile, global logistics disruptions continue to affect shipping reliability. Consulting firm Oliver Wyman reported that rerouting around the Red Sea and Cape of Good Hope has added roughly 8 to 15 days to some Asia-Europe shipping routes while increasing fuel and conflict-related surcharges.

This means that production planning for hardware startups now depends on variables that are often outside engineering control entirely.

Korea Is Treating Supply-Chain Stability as an Industrial Priority

South Korea is increasingly responding to these risks at policy level.

The country’s Framework Act on Support for Supply Chain Stabilization for Economic Securityaims to strengthen response capabilities against supply disruptions caused by domestic and overseas instability.

In April 2026, the Ministry of SMEs and Startups announced its first 2026 selection plan for supply-chain stabilization lead operators under the framework. The broader policy direction now includes support for import diversification, production-base expansion, stockpile strategies, and supply-chain resilience measures.

The Ministry of Trade, Industry and Energy has also expanded support programs targeting Korea’s materials, parts, and equipment sector, particularly for companies facing raw-material instability and restructuring pressure in global supply chains.

This shift reflects an important change inside Korea’s startup ecosystem. Supply-chain resilience is increasingly viewed as part of commercialization readiness itself, not simply an operational issue to solve later.

Investors Are Starting to Look Beyond Product Demos

As hardware sectors become more dependent on global semiconductor allocation, logistics reliability, and component availability, startups face growing pressure to prove they can manufacture consistently under unstable market conditions.

Kang believes scalability now depends on more than technical capability alone.

“The most important indicators are supply-chain stability, the existence of real purchasing customers, and a repeatable production structure.”

That shift matters not only for Korean startups, but for the broader global hardware ecosystem. In an environment shaped by AI-driven semiconductor competition, geopolitical uncertainty, and rising production costs, strong engineering alone no longer guarantees product survival.

The startups most likely to scale may not be the ones with the most impressive prototype. They may be the ones capable of continuing production when the supply chain itself becomes unstable.

Hardware Startups Are Entering an Era Where Supply Stability Determines Survival

Yes, the global hardware industry is no longer operating in a stable production environment.

Semiconductor allocation pressure, raw-material volatility, logistics disruption, and geopolitical uncertainty are increasingly shaping which products successfully reach the market and which quietly disappear before scale.

Hence, that shift is forcing startups, investors, and manufacturing partners to rethink what real commercialization readiness actually means.

Because in today’s hardware ecosystem, a strong prototype may open the door, but long-term survival increasingly depends on the ability to keep producing when the supply chain itself becomes unstable.

Key Takeaways

- Hardware startups can fail even after building technically strong products if supply conditions change before production begins.

- IC shortages, memory allocation pressure, and passive-component delays are creating growing risks for smaller hardware companies.

- The three-to-nine-month production window has become a critical vulnerability period for startups entering manufacturing.

- Supply-chain instability can destroy product economics, delay launches, and disrupt fundraising or customer commitments.

- South Korea is increasingly treating supply-chain resilience as a commercialization issue, not just a procurement problem.

- Investors are paying closer attention to repeatable production structures and supply stability, not only prototype performance.

- Global hardware startups now operate in a manufacturing environment shaped by AI-driven semiconductor demand, logistics disruption, and geopolitical instability.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.