A global fintech company entered South Korea with a model that had already proven successful across multiple Asian markets. Its cross-border payment and foreign exchange services were built for scale and standardization. Yet shortly after launch, operations stalled. Now, the issue was not in demand. It was that the model itself did not align with how Korea’s financial system is structured.

When a Proven Fintech Model Stops Working: A Case Study

Most of the time, global fintech expansion follows repeatable logic. Once a payment or remittance model proves successful across multiple markets, companies tend to scale it region by region with minimal structural changes.

Now, this approach may work in other parts of Asia. But in South Korea, the same assumption can break at the regulatory layer.

As discussion on Korea expansion challenge continues, Chris Song, Founder and Managing Partner at Hyesung Accounting & Advisory Corporation narrated a specific case example.

According to Chris Song, there was a moment when a company tried to deploy its existing global model without major adjustments. And this happened to a high-growth fintech operating across Asia, offering cross-border remittance and payment services. Not an early-stage experiment firm.

“At the initial stage of entry, the company sought to apply its global standard service model directly to the Korean market. However, this approach led to regulatory challenges, ultimately resulting in the suspension of its services,”

Song explained to KoreaTechDesk.

This moment is the core of the case. The model did not fail because of weak product-market fit. It failed because the operating design did not match Korea’s regulatory framework.

Why Payments and FX Are Structurally Different in Korea

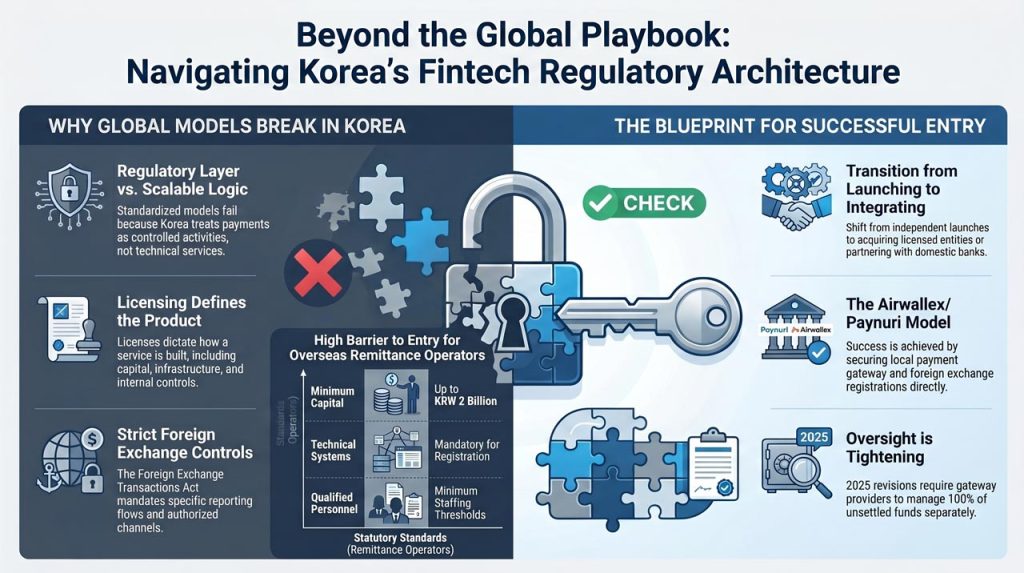

South Korea’s financial system treats cross-border payments and foreign exchange as controlled activities embedded within a regulatory framework, not just technical services.

The Foreign Exchange Transactions Act defines how foreign exchange transactions must be conducted, including classification of transaction types, reporting requirements, and how payments and receipts are processed. These rules shape how money moves, not just how it is recorded.

For fintech companies, this creates a structural constraint. A product designed to route funds seamlessly across jurisdictions must be rebuilt to comply with local transaction controls, reporting flows, and authorized channels.

Hence, this is where many global models break. Most global companies assume interoperability. But Korea requires specific regulatory integration.

Licensing Is Not a Formal Step. It Defines the Product

In Korea, financial services cannot operate outside defined licensing categories. The Electronic Financial Transactions Act requires payment-related businesses to obtain permission or registration, depending on the type of service.

This includes payment gateway services, electronic payment instruments, and settlement-related functions. Approval depends on capital, infrastructure, internal controls, and operational readiness.

For cross-border remittance, the bar is even more specific. Under Korea’s foreign exchange framework, small-amount overseas remittance operators must register with defined requirements, including minimum capital of up to KRW 2 billion, technical systems, and qualified personnel.

And these are not compliance details that can be handled later because they define how the service must be built from the start.

Song noted that this is where many fintech companies underestimate the challenge.

“Korea has a relatively stringent financial regulatory environment, particularly in areas related to foreign exchange and payment services, where licensing and compliance requirements are high.”

When Regulation Forces a Strategic Reset

After its initial model failed to operate within Korea’s regulatory environment, the company had to reconsider its entire approach.

Instead of adjusting parameters, it changed structure.

“The company began restructuring its business model by pursuing the acquisition of a licensed payment gateway company and establishing partnerships with local banks,”

Song said.

This shift reflects a broader pattern in Korea’s fintech market.

Rather than launching independently, foreign fintech firms often enter through:

- acquiring locally licensed entities

- partnering with domestic financial institutions

- aligning with existing regulatory frameworks

A recent example reinforces this pattern. In 2026, Airwallex acquired South Korean payments firm Paynuri, securing local licenses including payment gateway and foreign exchange registration. The move allowed the company to operate directly within Korea’s regulatory perimeter rather than relying on external intermediaries.

This is not just an isolated strategy. It is becoming a common entry pathway.

Korea Is Open to Fintech. But Within Defined Boundaries

South Korea has actively promoted fintech innovation through policy tools such as the Korea Financial Regulatory Sandbox.

Introduced in 2019, the sandbox allows new financial services to operate under regulatory exemptions while authorities evaluate their impact. As of recent data, more than 1,000 innovative financial services have been designated under the program.

However, the sandbox does not remove regulatory boundaries. Applications are reviewed based on consumer protection, financial stability, and risk management. Exceptions can be denied if they threaten market order or user safety.

This reinforces a key point.

Korea indeed supports fintech innovation, but not at the expense of financial system control.

Regulation Is Tightening, Not Loosening

Moreover, recent developments suggest that Korea’s financial oversight is becoming more structured as digital payments expand.

Following a major payment settlement issue involving domestic platforms, the Financial Services Commission introduced revisions to the Electronic Financial Transactions Act in 2025. These changes require payment gateway providers to separately manage 100 percent of unsettled funds and strengthen oversight mechanisms tied to transaction scale.

So, the direction is now clear.

As fintech activity grows, Korea is increasing supervision, especially in areas involving settlement risk and consumer protection. And for foreign fintech companies, this means entry barriers are not static. They gradually evolve along with market conditions.

The Real Lesson: Product-Market Fit Includes Regulation

Now, the fintech company in Song’s case did not fail because its product lacked value. It failed because its model assumed that regulatory environments could be treated as extensions of global operations.

Because apparently, that assumption did not hold in Korea.

“This case illustrates how unforeseen regulatory challenges at the execution stage can necessitate a fundamental adjustment of the initial business strategy,”

Song said.

And the adjustment itself was not minor. It required rebuilding the operating model around local licenses, partnerships, and regulatory expectations.

Why Korea Requires a Different Fintech Entry Mindset

Indeed, for global fintech operators, Korea presents a different kind of challenge.

It is not just about entry access but also about the alignment in the process.

Payment flows, FX handling, licensing scope, and institutional partnerships are tightly integrated into the financial system. And companies cannot assume that a product that works across multiple market will automatically function in Korea without structural changes.

This does not mean that Korea is inaccessible. It just makes it more structured.

With this, companies that approach Korea as a system to integrate tend to adapt successfully. Those that approach it as simply a market to deploy often encounter friction at the point of execution.

Local Licensing Is Not a Workaround. It Is the Model

Finally the most crucial lesson to learn is that Korea’s fintech operates within defined regulatory architecture.

So, global models that ignore this architecture must be redesigned.

Local licensing, partnerships, and regulatory alignment are not fallback options. They are often the only viable way to operate at scale.

For founders and investors evaluating Korea as part of an Asia-Pacific fintech strategy, this changes the entry question.

It is no longer how fast a product can be launched.

It is how quickly the business model can be rebuilt to fit the system it is entering.

Key Takeaway

- Global fintech models can fail in Korea when they are deployed without adapting to local licensing and regulatory structures

- Foreign exchange and payment services are tightly regulated, shaping how transactions must be designed and executed

- Licensing is not procedural but defines operational capability, infrastructure, and product scope

- Successful entry often requires local adaptation, including acquiring licensed entities or partnering with domestic financial institutions

- Korea supports fintech innovation through mechanisms like the regulatory sandbox, but within strict consumer protection and financial stability boundaries

- Regulatory oversight is increasing, particularly in payment settlement and risk management

- The structural core lesson: in Korea, regulatory fit is part of product-market fit, not a post-launch adjustment

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.