Many founders assume venture capital is the natural next step once a startup begins gaining traction. Yet strong products, growing customers, and even healthy revenue often fail to convince investors. Across global startup ecosystems, the issue is becoming increasingly visible: some companies are not rejected because they are weak businesses, but because they do not match the financial structure venture capital was designed to support.

Venture Capital Is Expanding, But the Market Is Narrowing

Global venture funding rebounded sharply in 2025, though the recovery was still concentrated heavily around a smaller group of companies.

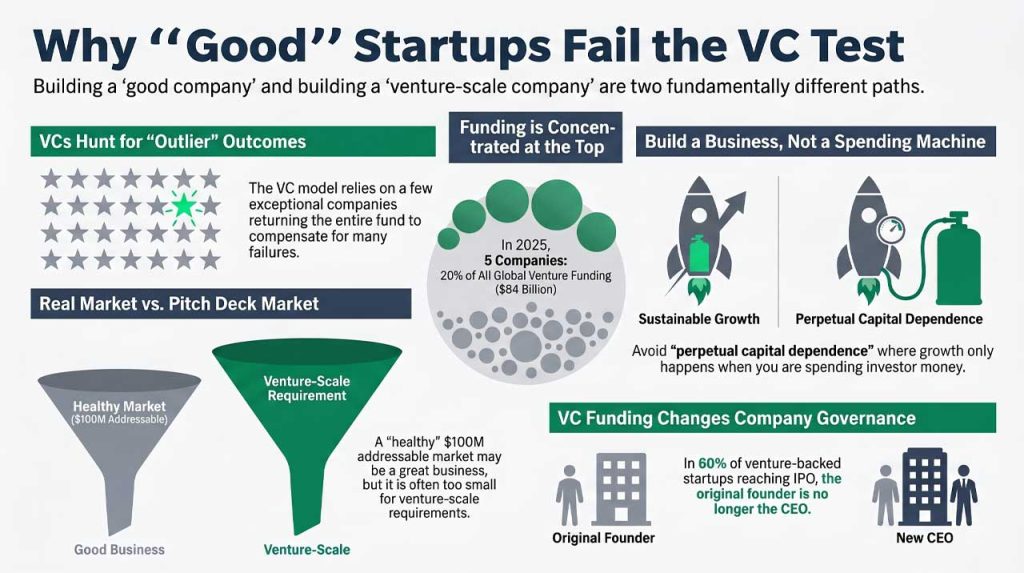

Crunchbase reported that global venture and growth investors deployed around USD 425 billion into more than 24,000 private companies in 2025, up roughly 30% year-over-year. However, five companies alone accounted for nearly USD 84 billion, representing about 20% of all venture funding globally. AI-related companies also absorbed roughly half of total global venture investment during the year.

Carta observed a similar pattern. While startup fundraising activity increased in 2025, total deal count fell to a six-year low as investors concentrated larger amounts of capital into fewer companies with stronger hypergrowth narratives.

Zooming in to South Korea, the venture market has also reflected the same broader shift.

According to the Ministry of SMEs and Startups (MSS), Korean venture investment reached KRW 13.6 trillion in 2025, the second-highest annual total on record. ICT services accounted for 20.8% of total investment, followed by bio and healthcare at 17.4% and electrical machinery and equipment at 14.6%.

At the same time, MSS stated that twelve designated “super-gap” sectors attracted KRW 5.2 trillion in venture investment, representing around 76% of total investment tracked under the government’s strategic industry framework.

The numbers show that while venture capital remains highly active, the structure of the market increasingly rewards companies capable of producing massive outcomes rather than simply becoming durable businesses.

Why Venture Capital Prioritizes Outlier Outcomes

Global investor and business advisor Igor Strečko, the Founding/Managing Partner at NeoZone Collective and Managing Director at Strecko Investment, believes many founders misunderstand what venture capital is fundamentally designed to do.

“Traditional VC does its job very well, for the type of companies it was designed for,”

Strečko told KoreaTechDesk during discussions on global startup M&A partnership and scale-up challenges.

“The model is built around broad portfolios, a high volume of investments, and the assumption that most companies will fail while a few exceptional outliers return the entire fund.”

That logic is deeply embedded into venture capital economics itself.

A National Bureau of Economic Research (NBER) study surveying 885 venture capitalists across 681 firms found that VC funds typically market returns around 3.5 times invested capital to limited partners. The same research showed that many venture firms evaluate opportunities primarily through potential exit multiples rather than traditional long-term cash flow models.

Harvard Business School research has also noted that venture capital operates best within a relatively narrow category of businesses capable of generating extremely large outcomes. Another HBS study examining startup investing described early-stage venture returns as heavily concentrated around rare outlier companies while many portfolio firms fail completely.

This creates a structural reality many founders underestimate: building a good company and building a venture-scale company are not always the same thing.

The Market Size Problem Investors Quietly Watch

One of the most common disconnects between founders and investors emerges around total addressable market assumptions.

“Many companies present a ‘USD 50 billion market’ in their pitch deck,”

Strečko explained.

“But once you break it down into a realistically addressable segment, for their specific product, in their actual geography, suddenly you are looking at a USD 100 million market.”

He then emphasized that this smaller market size does not necessarily make a business weak.

“That can still be an excellent business. It just may not be a venture-scale business.”

After all, venture funds mostly rely on a small number of breakout companies to generate enough returns. And that is especially crucial when they need to compensate for the many investments that fail or produce limited outcomes.

As a result, startups operating in specialized industries, geographically limited markets, or operationally intensive sectors often face a difficult fundraising environment even when the underlying business itself appears healthy.

This dynamic is becoming increasingly visible across global startup ecosystems as investors concentrate on funding around sectors capable of scaling aggressively, particularly artificial intelligence, deep technology, and platform-based businesses.

When Startups Become Machines for Raising Capital

Moreover, the growth itself can also become misleading. Strečko further cautioned,

“If growth depends entirely on raising the next funding round, without a visible path toward sustainable revenue generation, the company is not really building a business.

It is building a machine for spending investor money,”

And this observation reflects a broader tension increasingly discussed across global startup ecosystems.

In highly competitive funding environments, some companies optimize aggressively for fundraising momentum, user acquisition metrics, or valuation growth without developing sustainable economics underneath.

Now, this does not mean venture-backed growth is inherently unhealthy. Many transformative companies required years of aggressive investment before becoming profitable indeed.

But the distinction between strategic long-term investment and perpetual capital dependence is becoming even more important today, especially as global financing conditions tighten and investors place greater emphasis on efficiency and sustainable growth.

And this issue is especially relevant in South Korea as the country is aiming to become a top four global venture powerhouse. Policymakers have continued expanding support for venture investment and scale-up ecosystems. And Korea’s startup environment has become significantly more mature and globally connected over the past decade.

Still, larger pools of available capital also increase pressure on founders to understand what type of financing structure actually matches the long-term nature of their business.

Venture Capital Changes More Than Ownership

Not only that, but funding decisions also reshape governance itself.

Many founders initially focus on valuation, dilution percentages, or fundraising milestones. However, institutional capital changes how companies operate internally over time.

“Some founders intellectually understand that investors need equity participation, but emotionally they are not prepared for the consequences,”

Strečko further explained.

He pointed specifically to dilution, board authority, investor influence over management decisions, and leadership restructuring as common friction points.

Academic research also supports that shift. A large-scale study examining more than 18,000 venture-backed firms found that founders rarely maintain long-term control after institutional scaling. In nearly 60% of companies reaching IPO, the founder was no longer serving as CEO by the time the company went public.

Another study published in the Journal of Corporate Finance found that experienced repeat founders often negotiate more favorable governance structures and retain greater board influence compared with first-time entrepreneurs.

The findings reinforce a difficult reality many founders encounter late in the fundraising process: venture capital is not simply growth financing. It is institutional scaling capital that gradually transforms governance, accountability, and leadership expectations inside the company itself.

The Harder Question Behind Startup Funding

The modern startup ecosystem often treats venture funding as a universal validation mechanism. Yet many profitable, stable, and operationally healthy businesses may never fit traditional venture economics.

And that does not automatically make them failures.

Because in many cases, the mismatch comes from the structure of the funding model itself rather than the quality of the business.

As global venture markets continue concentrating around fewer high-growth sectors and increasingly large outcomes, founders may need to ask a more difficult question earlier in the company-building process: not simply whether investors want the business, but whether the business itself is structurally compatible with venture capital expectations.

For some startups, the answer may still be yes.

But for many others, sustainability, profitability, and long-term resilience may ultimately matter more than chasing a financing model built primarily for outlier-scale returns.

Key Takeaways

- Venture capital is designed for outlier-scale outcomes, not simply strong or profitable businesses.

- Global venture funding is becoming more concentrated around fewer companies and high-growth sectors such as AI and deep technology.

- A strong business can still fail the VC test if its realistic market size cannot support venture-scale returns.

- Capital-dependent growth creates long-term risk when companies rely primarily on future funding rounds instead of sustainable revenue generation.

- Venture funding changes governance structures, including board authority, founder control, and leadership expectations.

- South Korea’s expanding venture ecosystem increases the importance of capital-model fit as founders evaluate long-term growth strategies.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.