Korea proved during the COVID-19 pandemic that it could rapidly develop and export diagnostic products at global scale. Yet several years later, the country still faces a difficult question that extends far beyond innovation speed alone: why has Korea produced successful diagnostic companies, but not yet a long-term global diagnostics giant capable of competing at the level of Roche, Abbott, or Siemens Healthineers?

Korea Built Strong Diagnostic Skills, But Global Leadership Needs More

Korea’s diagnostics industry entered the global spotlight during the pandemic as local companies rapidly expanded production of COVID-19 test kits and exported them worldwide. The country’s manufacturing speed, engineering execution, and operational flexibility became highly visible during the emergency healthcare response.

However, the post-pandemic market reset has exposed a more structural challenge inside Korea’s diagnostics ecosystem.

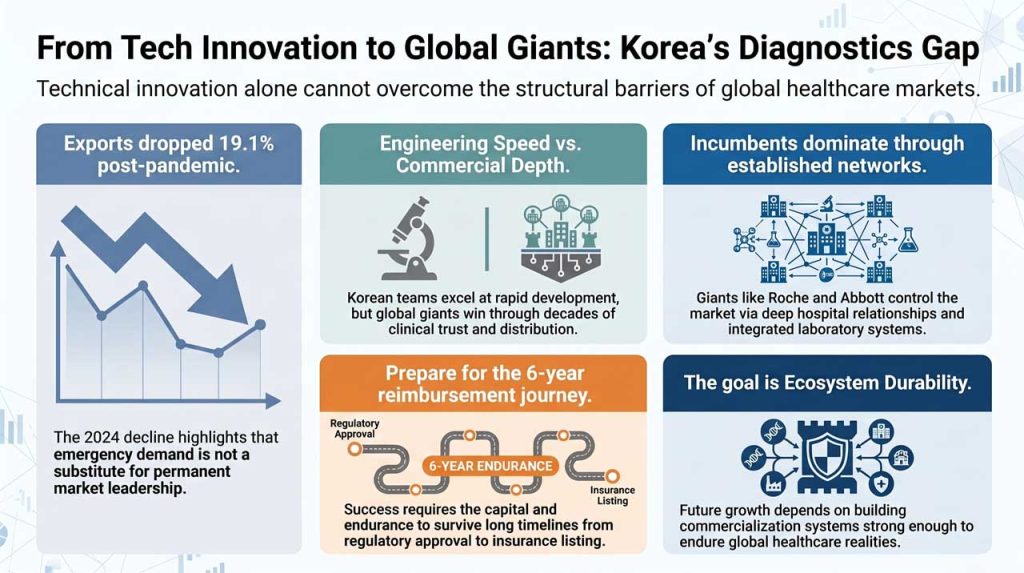

According to Korea’s national statistics portal, domestic production of in vitro diagnostic devices fell to KRW 997.3 billion in 2024, down 15.8% year over year. Exports also declined 19.1% to KRW 949.7 billion as global demand for COVID-19-related diagnostic products weakened.

The shift highlighted the reality that many healthcare investors and startups are now confronting globally. Emergency demand can rapidly expand diagnostic companies, but sustaining long-term international market leadership requires a much deeper commercialization infrastructure.

During a KoreaTechDesk discussion on the manufacturing and commercialization challenges of diagnostic startups, Hyou-Arm Joung, CTO and Co-Founder of Kompass Diagnostics, explained that Korea’s challenge is not a lack of technical capability.

“Korea has very strong foundational infrastructure for diagnostic development compared to many other countries, including strengths in manufacturing capability, operational efficiency, and experienced production talent.”

He said Korean teams often move quickly during early-stage development and engineering execution.

“Korean teams often perform very well in early-stage innovation, rapid development, engineering execution, and manufacturing adaptation.”

The Real Gap Appears During Global Commercialization

Despite Korea’s technical strengths, Joung believes the industry still faces a structural disadvantage when competing globally.

“However, when moving toward global commercialization, one major challenge is the absence of large-scale global diagnostic leaders originating from Korea.”

The issue becomes clearer when comparing Korea’s ecosystem against the scale of global diagnostics incumbents.

Roche reported CHF 13.8 billion in Diagnostics division sales in 2025. Abbott reported USD 8.94 billion in diagnostics revenue during the same year. These companies operate through decades-old hospital relationships, reimbursement networks, regulatory infrastructure, installed laboratory systems, and post-market support organizations spread across global healthcare systems.

In diagnostics, scale is not simply about manufacturing volume. It is about maintaining long-term trust across regulators, hospitals, insurers, laboratories, physicians, and healthcare providers simultaneously.

And that infrastructure takes years or even decades to build, just like Joung explained.

“In diagnostics, the market has historically been led by companies such as Roche, Abbott, Siemens, and other large multinational players that have accumulated decades of capital, regulatory experience, distribution networks, manufacturing maturity, and clinical trust.”

Diagnostic Markets Structurally Favor Large Incumbents

The diagnostics sector also operates differently from many software-driven startup markets because incumbents can continuously absorb emerging technologies into existing commercial ecosystems.

In November 2025, Abbott agreed to acquire Exact Sciences in a deal valued at up to USD 23 billion, strengthening its cancer diagnostics portfolio. Roche also announced the acquisition of digital pathology company PathAI in May 2026 to expand its AI-enabled diagnostics capabilities.

The pattern reflects how major diagnostics companies often expand through platform acquisition and integration rather than allowing smaller challengers to independently dominate global markets.

Joung believes this creates a difficult structural environment for startups trying to scale independently.

“In many cases, technical innovation alone is not enough to overcome the realities of global commercialization, regulatory expansion, manufacturing scale-up, reimbursement systems, and long-term operational sustainability.”

The challenge extends beyond technology itself. Diagnostics companies entering international markets must navigate reimbursement systems, country-specific healthcare regulations, clinical validation requirements, coding structures, payer negotiations, and post-market monitoring obligations.

In the United States alone, diagnostic commercialization often requires navigating FDA regulatory pathways alongside reimbursement systems administered through Medicare and private insurers. Europe’s In Vitro Diagnostic Regulation (IVDR) has also significantly increased compliance and validation requirements across the European diagnostics market.

For startups, these layers create both financial and operational pressures that are often far larger than early product development itself.

Korea Is Trying to Strengthen the Missing Infrastructure

Korea’s government has already acknowledged many of these structural commercialization gaps.

The Ministry of Health and Welfare previously announced a five-year medical-device industry development plan aimed at shifting Korea from a technology-following structure toward a more globally competitive medical-device ecosystem. The strategy includes support for clinical demonstration, regulatory improvement, R&D commercialization, and market expansion.

Korea has also continued refining domestic regulatory systems for medical devices and diagnostics. Earlier this year, the country introduced an Immediate Market Entry pathway allowing certain eligible medical devices to enter the market without undergoing separate new health technology assessment procedures.

The pathway applies to 199 categories, including 83 in vitro diagnostic reagents, and may shorten domestic market-entry timelines significantly for qualifying products.

Still, faster domestic approval systems alone do not automatically solve global commercialization challenges.

A 2026 study published in the Journal of Korean Medical Science found that the median time required for medical technologies in Korea to move from approval to reimbursement listing reached six years overall. Even moderate- to high-risk technologies requiring premarket approval faced substantial timelines before reimbursement integration.

Now, for healthcare startups, reimbursement endurance can become just as important as technical innovation.

Korea’s Next Diagnostics Challenge Is Institutional, Not Technical

Korea has already demonstrated that its diagnostics sector can innovate quickly under pressure. The harder challenge now is building long-term industrial ecosystems capable of sustaining global competitiveness beyond crisis-driven demand cycles.

That requires more than strong engineering teams or manufacturing speed alone. It requires reimbursement strategy, regulatory endurance, global distribution infrastructure, long-term clinical trust, post-market support systems, and sustained capital investment across multiple markets simultaneously.

Joung believes this broader ecosystem maturity remains one of the industry’s biggest hurdles.

“The challenge is building the long-term industrial ecosystem, capital scale, regulatory endurance, and commercialization infrastructure necessary to compete globally over time.”

As healthcare systems continue decentralizing diagnostics and expanding point-of-care testing globally, Korea’s diagnostics industry may now be entering a more difficult phase. The next challenge is no longer proving that Korean companies can innovate. It is proving they can build institutions capable of surviving global healthcare markets over the long term.

Korea’s Global Diagnostics Ambition May Depend on Ecosystem Depth

Finally, the diagnostics industry increasingly rewards companies capable of managing regulation, reimbursement, manufacturing, clinical trust, and healthcare-system integration simultaneously across multiple countries.

Korea already possesses many of the technical ingredients necessary for innovation. Yet global leadership in diagnostics has historically depended on something larger than technology itself: ecosystem durability.

Therefore, for Korean diagnostic startups, the path toward becoming global giants may ultimately depend less on discovering the next breakthrough sensor and more on building commercialization systems strong enough to endure the realities of global healthcare infrastructure.

Key Takeaways

- Korea has strong diagnostic engineering and manufacturing capability, but global diagnostics leadership requires broader commercialization infrastructure.

- Korean teams perform strongly in early-stage innovation, rapid development, and manufacturing adaptation.

- Korea still lacks large-scale global diagnostics leaders with the ecosystem depth of Roche, Abbott, or Siemens Healthineers.

- Global diagnostics markets structurally favor incumbents because large companies already possess regulatory networks, reimbursement access, hospital relationships, and clinical trust built over decades.

- Korea’s diagnostics industry experienced a significant post-pandemic export slowdown, with 2024 in vitro diagnostic exports falling 19.1% year over year.

- Regulatory approval alone is not sufficient for globalization. Diagnostic startups must also manage reimbursement systems, clinical validation, post-market obligations, and long-term operational sustainability.

- Joung believes Korea’s next diagnostics challenge is increasingly institutional rather than technical, requiring deeper ecosystem maturity to compete globally over time.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.