For years, discussions around critical minerals largely revolved around securing enough raw materials to keep factories running. Today, that conversation is changing. As geopolitical uncertainty, export controls, and concentrated processing capacity reshape global supply chains, the question is no longer simply how Korea can obtain critical minerals. It is how resilient its industrial ecosystem can become when access grows increasingly uncertain.

Korea’s Industrial Competitiveness Starts Long Before Manufacturing

South Korea’s reputation as a global leader in semiconductors, rechargeable batteries, advanced manufacturing, robotics, and defense technologies often draws attention to innovation happening inside laboratories and production facilities. Less visible is the network of mines, refiners, processors, logistics operators, and recycling systems that quietly supports those industries.

As governments around the world reassess economic security through the lens of critical minerals, Korea is also repositioning its strategy. Rather than treating mineral procurement as a procurement issue alone, policymakers are increasingly building broader resilience across sourcing, recycling, monitoring, and overseas partnerships.

Steve Jung, President of the Korea Mineral Resource Industry Association, views the issue through the lens of an industry organization that represents companies involved in resource development, mineral trading, and metal recycling across South Korea.

His work also focuses on resource supply-chain management and overseas resource development, placing him at the intersection of industrial policy discussions and the practical challenges companies face in securing critical minerals.

Against that backdrop, Jung believes many companies still underestimate where today’s supply-chain risks have shifted.

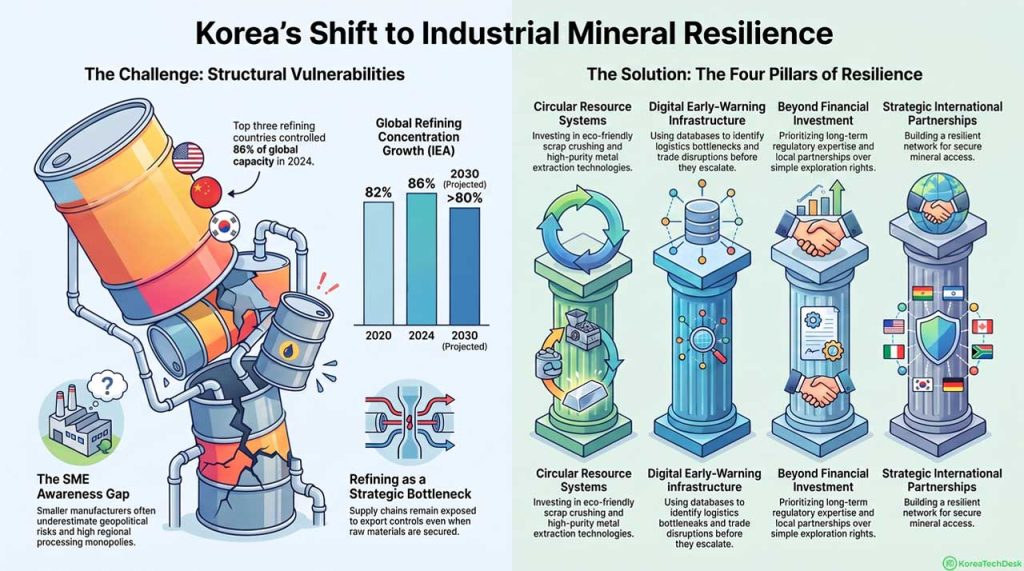

“Many SMEs often focus primarily on direct raw material costs and stable immediate delivery, sometimes underestimating the geopolitical risks and the high concentration of refining and processing capacities in specific regions.”

And his observation points to a broader shift affecting industrial economies. Reliable access to critical minerals increasingly depends not only on resource availability but also on refining capacity, geopolitical developments, logistics resilience, and evolving trade policies.

As governments and manufacturers strengthen supply-chain resilience, these upstream factors are becoming more of strategic considerations rather than mere operational concerns.

Refining Concentration Has Become a Strategic Risk

Building on these evolving interests, the challenge now extends well beyond mining.

According to the International Energy Agency’s Global Critical Minerals Outlook 2025, refining remains even more geographically concentrated than mining for many strategic minerals. The report found that the combined share of the world’s three largest refining countries increased from 82% in 2020 to 86% in 2024. Even under projected market expansion, that concentration is expected to remain above 80% well into the next decade.

Such concentration creates vulnerabilities that extend throughout manufacturing supply chains. Companies may secure mineral supply contracts, yet remain exposed if processing capacity becomes constrained by export controls, geopolitical disputes, or operational disruptions.

Recent developments have reinforced those concerns. China continues to play a dominant role across multiple critical mineral processing segments while tightening export-control mechanisms covering several strategic materials. These policy changes have prompted governments and manufacturers worldwide to diversify sourcing strategies and strengthen supply-chain resilience.

Hence, for Korean manufacturers, the challenge is not simply identifying new suppliers. It is understanding where dependence exists across every stage of the value chain.

Overseas Resource Development Demands More Than Investment

Diversifying mineral sources has become a major policy objective for many economies, including Korea. Yet expanding overseas resource development involves far more than securing exploration rights or financing new projects.

Jung noted that execution often proves far more difficult than strategy.

“The most common challenges lie in navigating complex local regulatory frameworks, establishing reliable local partnerships, and securing long-term logistics infrastructure amidst fluctuating global market policies.”

Those challenges illustrate why overseas resource development remains a long-term capability rather than a short-term procurement solution.

Recognizing these realities, the Korean government has expanded financial support for overseas resource development while strengthening international cooperation with resource-producing countries.

Not only that, but official policy also emphasizes early-risk identification, public-private collaboration, and diversified sourcing to reduce excessive dependence on any single market.

And such efforts reflects the country’s acknowledgement that resilient supply chains depend as much on trusted partnerships and institutional coordination as they do on access to mineral deposits.

Recycling Is Becoming Part of Industrial Resilience

At the same time, resource security increasingly extends beyond extracting new materials.

Korea has identified recycling as another pillar of its critical minerals strategy, reflecting broader global efforts to build circular supply chains for strategic resources. Rather than viewing recycling primarily as an environmental initiative, policymakers increasingly regard it as an industrial capability that can improve long-term resource security.

Jung sees practical opportunities emerging alongside these policy priorities.

“The most realistic opportunities for startups lie in advanced, eco-friendly processing technologies, such as scrap crushing and high-purity metal extraction, especially driven by tightening global ESG mandates and circular economy regulations.”

His perspective aligns with Korea’s broader policy direction, which includes expanding recycling capacity for strategic minerals, supporting advanced processing technologies, and strengthening resource circulation systems.

Still, recycling alone cannot eliminate supply-chain vulnerabilities. Collection systems, processing efficiency, technology maturity, and economic viability remain important challenges that determine commercial success.

Digital Visibility Is Becoming Just as Important as Physical Supply

Now, supply-chain resilience increasingly depends on information as much as physical inventory.

Governments and industrial companies are investing in digital monitoring systems capable of identifying concentration risks, trade disruptions, logistics bottlenecks, and geopolitical developments before they escalate into operational problems.

Korea’s latest critical minerals policies include expanded supply-chain databases, early-warning mechanisms, and monitoring capabilities designed to improve visibility across increasingly complex global value chains.

And Jung believes digital infrastructure will become one of the defining competitive advantages over the coming years.

“Technology safeguarding, source diversification for critical minerals like tungsten and boron, and digital infrastructure for supply-chain monitoring will become paramount for maintaining industrial resilience.”

His comments suggest that future competitiveness will rely not only on securing materials but also on understanding vulnerabilities throughout the supply chain before they become crises.

Industrial Resilience Is Becoming Korea’s Next Competitive Advantage

The conversation surrounding critical minerals has matured considerably.

Only a few years ago, much of the attention focused on securing adequate supplies to support battery manufacturing and semiconductor production. Today, resilience encompasses geopolitical awareness, refining concentration, overseas partnerships, recycling capabilities, digital monitoring, and long-term strategic planning.

That broader perspective matters because industrial competitiveness increasingly depends on the ability to anticipate disruption rather than simply react to shortages.

That is why for founders developing industrial technologies, manufacturers expanding globally, investors evaluating supply-chain exposure, and policymakers designing long-term industrial strategies, critical minerals are no longer a narrow resource issue. They have become part of the infrastructure supporting Korea’s innovation economy.

Looking Beyond the Next Supply Disruption

Critical minerals rarely dominate public attention until shortages emerge or geopolitical tensions interrupt supply. Yet resilience is built long before disruption occurs.

As Korea strengthens its industrial ecosystem, the most durable competitive advantage may come from improving visibility across supply chains, strengthening trusted international partnerships, expanding recycling capacity, and recognizing that resilience begins well upstream of the factory floor.

Key Takeaway

- Industrial resilience now extends beyond mineral procurement to include refining capacity, logistics, partnerships, recycling, and digital monitoring.

- Many SMEs still underestimate geopolitical exposure and processing concentration, leaving them vulnerable to disruptions in increasingly complex supply chains.

- Refining concentration remains one of the most important structural risks within global critical mineral supply chains, according to the International Energy Agency.

- Overseas resource development requires long-term institutional capability, including regulatory expertise, trusted local partnerships, and resilient logistics.

- Recycling and advanced processing technologies are becoming increasingly important as Korea strengthens circular resource systems.

- Digital supply-chain monitoring is emerging as strategic infrastructure, helping governments and industries identify risks before they disrupt production.

- Korea’s critical minerals strategy increasingly reflects industrial resilience rather than procurement alone, offering lessons for founders, manufacturers, investors, and global ecosystem partners evaluating long-term competitiveness.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.