The Control Layer Behind Enterprise AI — Enterprise AI no longer moves through a single team or a single product. Once companies push beyond pilots, deployment involves platform vendors, system integrators, advisory firms, and internal business units working at the same time.

That shift is changing a basic assumption. The question is no longer only which technology a company adopts. It is who aligns the actors responsible for turning that technology into a working system.

Enterprise AI Is Becoming an Ecosystem Execution Problem

Global data shows how quickly AI has spread inside organizations. McKinsey’s latest State of AI research indicates that a large majority of companies now use AI in at least one business function, yet only about one-third report scaling those efforts across the organization.

The gap reflects a deeper change. AI is no longer a standalone capability. It depends on how organizations design workflows, structure delivery, and manage operations across teams.

Deloitte adds that 69% of enterprises expect implementing AI governance to take more than a year. That timeline highlights the complexity of aligning technical, regulatory, and operational requirements.

As AI moves into production environments, execution becomes distributed. Responsibility is shared across multiple parties, and that changes where control sits.

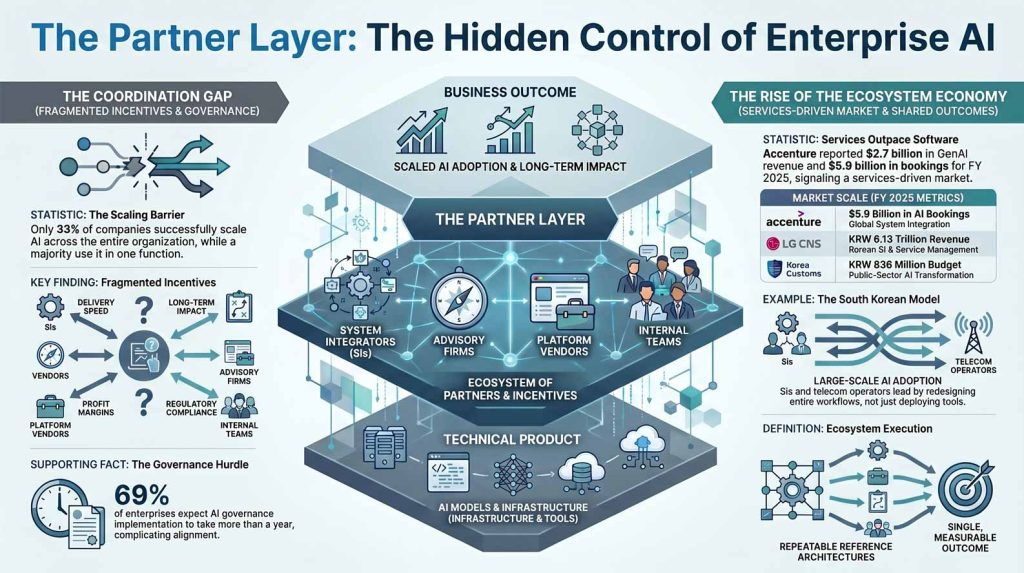

The Hidden Control Layer — Where Outcomes Are Actually Decided

As discussion on the complexity of enterprise AI continues, another crucial aspect to point out beyond its technical factors is the organizational capabilities.

Joseph Bosco, Partner Manager for Professional Services Asia Pacific-Japan (APJ) at Databricks, points to a specific pattern during an interview with KoreaTechDesk,

“One recurring issue is that the partner ecosystem is not aligned around the same outcome.”

He then elaborated that partners involved in a single project often operate with different priorities. One may focus on delivery speed, another on expanding advisory scope, while the enterprise expects a measurable business impact.

Hence, without early alignment on ownership and outcomes, execution can begin to drift even when the underlying technology is working as intended.

This reflects a structural reality. Enterprise AI projects often involve:

- system integrators responsible for delivery

- advisory firms shaping scope and strategy

- platform vendors providing infrastructure

- internal teams managing risk, data, and operations

Each group works toward different priorities. Without alignment, no single actor owns the final outcome.

OECD research supports this pattern, noting that fragmented governance and unclear responsibilities frequently slow execution even when technical capabilities are in place.

The result is not a failure of technology. It is a failure of coordination.

Why Even Leading AI Companies Depend on System Integrators

The growing influence of partners is also visible at the global level.

According to OpenAI as cited in Reuters, enterprise adoption of its Codex system is being expanded through collaborations with consulting and system integration firms such as Accenture, Capgemini, Cognizant, Infosys, PwC, and Tata Consultancy Services.

This shows that even frontier AI providers rely on partners to integrate systems into enterprise environments.

The economics reinforce this trend. Accenture reported USD 2.7 billion in revenue from generative and agentic AI and USD 5.9 billion in related bookings in fiscal 2025, supported by a workforce of around 77,000 AI and data specialists and more than 6,000 AI-related projects.

These figures suggest that enterprise AI is not only a software market. It is also a services-driven execution market where partners shape deployment outcomes.

South Korea’s AI Market Highlights the Partner Dynamic

South Korea provides a clear view of how this dynamic plays out in practice.

Local ICT companies, including telecom operators and system integrators, have been increasingly focusing on B2B AI as a primary growth area, according to reporting by Yonhap News Agency. The enterprise segment is emerging as a key battleground for AI monetization.

At the same time, large-scale public-sector projects show how AI adoption is structured.

The Korea Customs Service launched an AI transformation planning initiative in 2026 with a budget of KRW 836 million and a roadmap extending to 2029. The project is designed not only to deploy specific AI tools, but to redesign workflows, data systems, and operational structures across the organization.

This approach illustrates how AI is implemented in Korea. It is not limited to isolated use cases. It involves system-level integration that requires coordination across multiple stakeholders.

Major IT service firms are adapting to this environment. LG CNS reported KRW 6.1295 trillion in revenue in 2025 and highlighted its focus on strengthening system integration and service management capabilities as the market moves toward more advanced AI deployment.

These developments indicate that system integrators are becoming central to how AI is delivered and operated in Korea.

The Trade-Off — Speed of Execution Versus Control of Outcomes

The growing role of partners creates both advantages and risks.

On one side, system integrators and consulting firms enable faster deployment. They bring experience in large-scale integration, established delivery processes, and the ability to coordinate complex projects.

On the other side, reliance on external partners can reduce internal ownership.

If delivery models, governance structures, and operational responsibilities are not clearly defined, enterprises may struggle to maintain control over how AI systems evolve after deployment.

Bosco’s observation highlights this tension. When incentives diverge, projects can drift even when the underlying technology is sound,

“If those incentives are not aligned early, the project can drift even when the core technology is sound.”

In Korea, where enterprise structures are strong and SI-led delivery models are well established, this balance becomes particularly important.

That’s because the same ecosystem that accelerates execution can also shape the direction of that execution.

What This Means for Founders, Investors, and Global Operators

The rise of partner-driven execution is reshaping how enterprise AI markets operate.

For founders, building a strong product is no longer enough. In markets like South Korea, where system integrators play a central role, reaching enterprise customers often depends on how well a company fits into existing delivery ecosystems. Integration strategy becomes part of the product itself.

Investors are also adjusting their lens. Technical capability remains important, but it is no longer sufficient on its own. Companies that can navigate partner networks and retain influence over how their solutions are deployed tend to show stronger long-term positioning.

Meanwhile, enterprises entering Korea face a similar reality. Choosing the right technology stack is only one part of the decision. Understanding how system integrators operate, how responsibilities are shared, and how long-term ownership is defined often determines whether deployment succeeds beyond the initial phase.

These dynamics point to a broader shift. Enterprise AI no longer depends solely on what is built, but on how it is delivered, coordinated, and sustained over time.

Control in Enterprise AI Is Being Redefined

Enterprise AI is moving into a phase where outcomes depend less on the technology itself and more on how it is delivered and operated. As deployments scale, control shifts toward the ecosystem of partners that integrate systems, manage execution, and sustain operations.

In South Korea and across the Asia-Pacific region, this partner layer is becoming central to how AI is implemented.

Because AI success is no longer just about building the right model. Now, it also depends on how well organizations align internal teams, system integrators, and delivery models to turn AI into a working, reliable system.

As Bosco said,

“The stronger partners are the ones who have moved beyond bespoke work and built repeatable reference architectures, accelerators and governance models.”

Key Takeaway

- Enterprise AI scaling increasingly depends on partner alignment, not only technology capability

- Misaligned incentives across system integrators, vendors, and enterprises can stall deployment

- Global AI companies are relying on consulting and SI firms to integrate AI into enterprise systems

- Accenture reported $2.7B in generative AI revenue and $5.9B in bookings in 2025, reflecting the growth of AI services

- South Korea’s enterprise AI market is driven by B2B deployment through telecom, platform, and SI firms

- Public-sector AI projects in Korea emphasize system-level integration and long-term operational design

- Partner ecosystems can accelerate AI adoption but also influence control over outcomes

- Enterprise AI is shifting from product competition to ecosystem execution and delivery strategy

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.